#20 Micro-savings for Macro Impact: Unpacking SEBI’s Sachetized Mutual Fund Proposal for Financial Inclusion

Exploring how SEBI’s ‘sachetized’ mutual funds empowers first-time investors, accelerates socio-economic resilience, and charts a new roadmap for inclusive finance in India.

In today’s post, we delve into a critical financial policy development in India, one that could redefine how low-income communities gain access to formal investment products—specifically, mutual funds.

On January 22, 2025, the Securities and Exchange Board of India (SEBI) released a Consultation Paper titled “Promoting Financial Inclusion Through Sachetisation of Investment in Mutual Funds.” The term “sachetisation,” borrowed from consumer goods marketing, implies offering a product in micro or “sachet-sized” quantities to break down barriers to entry. SEBI’s paper aims to foster financial inclusion, inculcate the habit of systematic saving, and accelerate mutual fund investments among underserved segments by introducing a small-ticket Systematic Investment Plan (SIP) of INR 250 per installment (the “Small Ticket SIP”).

But is this initiative enough to create a real impact? How does it compare with global microsavings initiatives? What are the critical enablers, and what blind spots remain? And ultimately, what could be the socio-economic ripple effects of offering mutual funds in sachet form? Over the course of this long-form analysis, we will explore:

Microsavings through mutual funds as a pathway for financial inclusion

Global examples and lessons from similar initiatives

Key enablers of success in scaling micro savings

A deep dive into SEBI’s Consultation Paper

Identifying the gaps in the paper

Recommended enhancements, especially those touched upon in Annexure A

Potential pitfalls or elements to omit

Intended and unintended consequences for low-income communities in both rural and urban India

By unpacking these dimensions, we aim to provide a thorough analysis of the promise and limitations of “sachetized” mutual funds in driving financial inclusion in India.

2. Microsavings Through Mutual Funds: A Pathway for Financial Inclusion

2.1 Defining Microsavings

Microsavings refers to small, periodic deposits made by individuals typically belonging to low—or moderate-income segments. These savings might be as low as a few dollars (or a few hundred rupees) at a time, yet they accumulate into a substantial safety net over the long term. The traditional vehicles for micro-savings have been informal channels: self-help groups (SHGs), rotating savings clubs, or cooperatives. Just last year, India completed 30 years of the National Rural Livelihoods Mission, a landmark achievement in formalizing over 8.3 million SHGs, with a membership of over 85 million rural women across India. However, with the advent of technology and more sophisticated financial regulations, formal institutions and products have begun catering to this segment.

2.2 Why Mutual Funds?

Historically, mutual funds were perceived as a product for middle- or high-income earners—people who have disposable income to invest in a diversified portfolio. Yet the basic philosophy of mutual funds—to pool money from many investors and deploy it under professional management—perfectly aligns with the financial needs of low-income segments. By investing in mutual funds, participants can:

Spread Risk: Diversification is a core advantage of mutual funds, especially critical for low-income individuals who cannot afford large losses in a single asset.

Benefit from Professional Management: Few in underserved segments have the financial literacy, time, or resources to manage an investment portfolio. A mutual fund structure outsources that responsibility to professional asset managers.

Earn Market-Linked Returns: While savings accounts offer safety, their returns often fail to keep pace with inflation. Mutual funds, when chosen judiciously, can offer a better balance between risk and return.

2.3 The Roadblocks to Including Low-Income Investors

Despite these advantages, mutual funds remain under-penetrated in low-income communities for reasons such as:

Affordability Barriers: Minimum investment amounts are often too high, discouraging potential entrants.

Transactional Costs and Bureaucracy: KYC norms, paperwork, and brokerage fees can deter new investors.

Lack of Trust and Financial Literacy: Traditional communities often distrust formal financial systems, preferring local, informal options.

By enabling an SIP of just INR 250 per month, SEBI’s new proposal attempts to dismantle affordability barriers and encourage first-time formal market participation.

3. The Global Landscape: Lessons from Abroad

Microsavings programs have flourished globally, demonstrating that when you reduce barriers to entry, even the most financially vulnerable groups can participate and benefit. Below are select examples:

3.1 Kenya: M-Pesa and Mobile Savings

Kenya revolutionized mobile payments through M-Pesa, setting the stage for micro-savings accounts. Many Kenyan fintechs now offer incremental saving and micro-investment functions, allowing users to deposit small amounts directly from their mobile wallets. A noteworthy spillover is the partnership between M-Pesa and local money market funds, enabling micro-investments at scale.

3.2 Indonesia: TabunganKu

In 2010, Bank Indonesia launched TabunganKu (translating to “My Savings”), a nationwide micro-savings program with low minimum deposits, zero monthly fees, and minimal requirements for account opening. By harmonizing regulations across multiple banks, the initiative successfully brought millions of Indonesians into the banking fold—laying a foundation for more advanced investments like small SIPs in mutual funds.

3.3 Philippines: CARD Mutually Reinforcing Institutions (CARD MRI)

CARD MRI is a network of microfinance and mutual benefit associations. While it primarily focuses on microloans, it has also introduced products that function like micro-savings in mutual funds, pooling funds from members and investing them in local markets. The program underscores how group-based trust mechanisms can reduce default risk and administrative overhead.

3.4 United States: Individual Development Accounts (IDAs)

IDAs were designed to help lower-income Americans build assets for predefined goals (e.g., home purchase, education). While not directly invested in mutual funds, the concept shares similarities: structured savings matched by external contributors (often nonprofits or government). Some IDA programs eventually pivoted toward mutual fund-based savings plans, reinforcing how well-targeted incentives can move the needle on micro-savings behavior.

The underlying common theme of these examples is that all these initiatives hinge on ease of access, low transaction costs, and education/trust-building. While the regulatory context differs across countries, the overarching lesson is that lowering the barriers—whether through mobile channels, cross-subsidies, or specialized KYC processes—can have an outsized impact on financial inclusion.

4. Enablers of Success for Microsavings Initiatives

Scaling micro-savings programs, especially those linked to formal mutual funds, demands more than regulatory approval. Below are the multi-dimensional enablers that have repeatedly emerged as success factors globally:

Digital Technology Adoption:

Mobile-based platforms, e-wallets, or user-friendly apps can drastically reduce operating costs and boost convenience for low-income investors. UPI autopay in India, for instance, is a game-changer that allows seamless micropayments.Appropriate Regulatory Framework:

Regulations must permit small-ticket investments while keeping compliance processes manageable. SEBI's proposal to offer PAN exemptions up to a certain annual limit for small-ticket SIPs is a step in this direction.Trust and Awareness Building:

Low-income communities often distrust formal finance. Ongoing financial literacy, local language support, and community partnerships are paramount.Innovative Cost Structures and Incentives:

Traditional brokerage fees can make small-ticket investments economically unviable for fund houses and distributors. Offering discounted platform fees, reimbursing KYC costs, and providing distributor incentives can collectively close this gap.Robust Infrastructure:

From payment gateways to strong broadband networks in remote areas, robust infrastructure ensures cost efficiencies and user-friendly experiences.Long-Term Vision and Political Will:

Policy interventions for financial inclusion often require time to bear fruit. Regulatory bodies must remain committed, possibly mandating lower fees, or supporting expansions in remote areas.

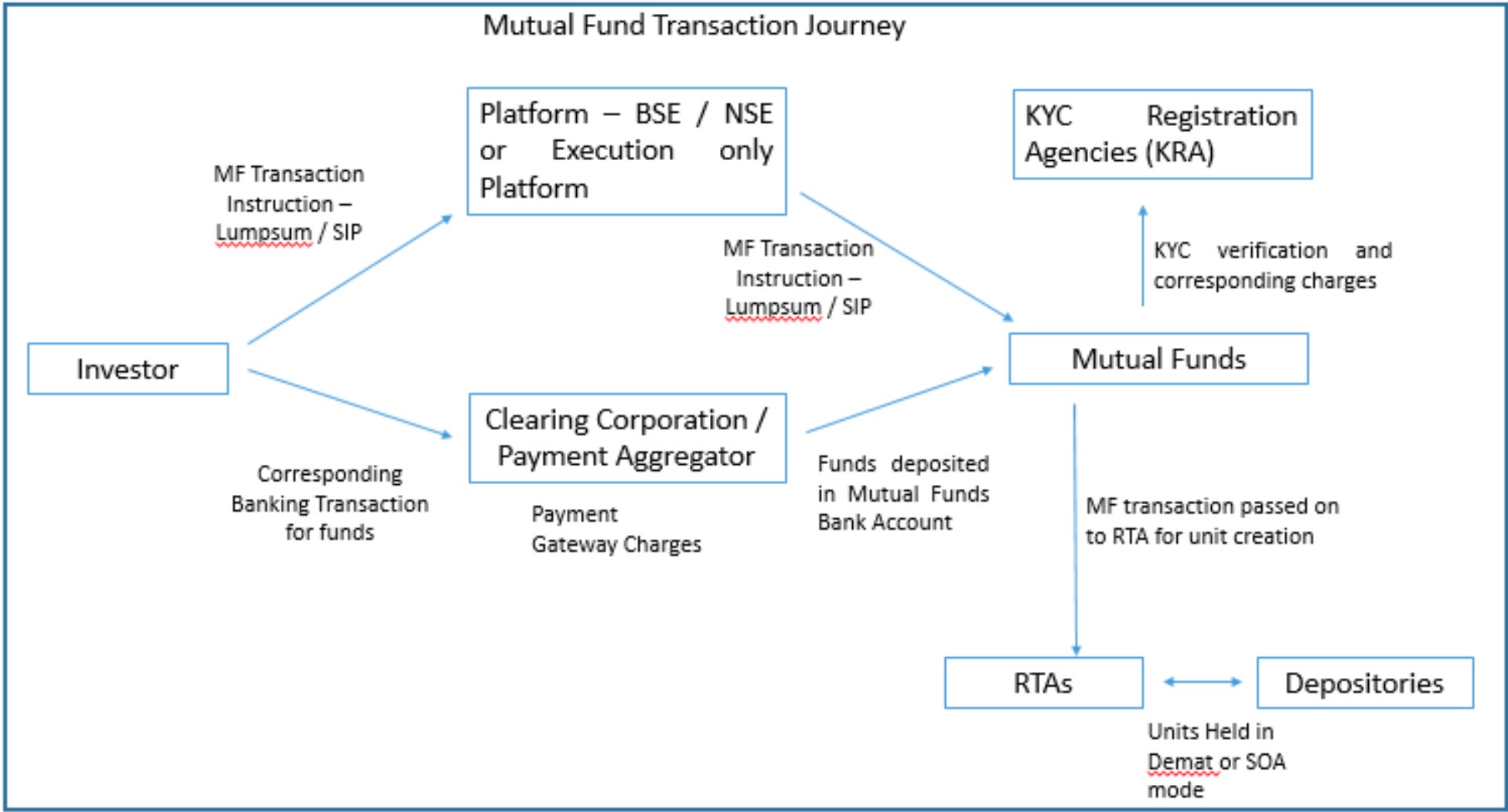

5. Deep Dive into the SEBI Consultation Paper

On January 22, 2025, SEBI issued a Consultation Paper on promoting financial inclusion via the “sachetisation” of mutual fund investments. Below is a distilled overview of the main points:

5.1 Objective and Rationale

Primary Goal: Facilitate “sachet-sized” mutual fund investments to promote systematic saving and financial inclusion for low-income groups.

Small-Ticket SIP: A monthly installment of INR 250, restricted to three SIPs per investor at the industry level, i.e., one SIP per AMC (up to three AMCs).

5.2 Key Proposals from SEBI

Growth Option Only

Small ticket SIPs should be available only in the Growth option. This ensures compounding benefits, though it also means no regular dividends for immediate liquidity.Exclusion of Certain Schemes

Debt schemes, Sectoral & Thematic Schemes, Small-cap, and Mid-cap are excluded. This presumably mitigates risks for first-time investors, focusing them on more diversified equity or balanced options.Mode of Payment

Only NACH or UPI autopay can reduce high transaction gateway fees and potential complexities.KYC and PEKRN

The Investor Education and Awareness (IEA) Fund can reimburse KYC costs for these small-ticket investments.

PAN-exempt KYC Registration Numbers (PEKRN) are permitted up to INR 50,000 per investor, per mutual fund, per financial year—lowering hurdles for those without PAN cards.

Distributor Incentive

A one-time incentive of INR 500 is payable to distributors who successfully onboard an investor that stays invested for 24 monthly installments (or 12 fortnightly installments). This aims to offset the minimal commissions from such small ticket sizes.Commitment Period

SEBI proposes a 5-year commitment, but investors can exit anytime without penalty, adhering to open-ended mutual fund norms.Disclosures and Communication

Mandatory use of registered mobile numbers for statutory disclosures. Email is optional, but text-based links to more detailed disclosures must remain active.

5.3 Why Sachetisation Now?

India’s Growth Story in Mutual Funds

Assets Under Management (AUM) have grown significantly, from INR 10 trillion in 2014 to INR 68.08 trillion in late 2024. However, penetration remains skewed toward urban, middle-, and high-income segments.Cost-Break Even Analysis

SEBI and industry participants predict that these small-ticket SIPs could break even for AMCs in two years with subsidized fees and partial cost reimbursement.

6. Where the Consultation Paper Falls Short

While SEBI’s push for sachetized mutual funds is laudable, certain aspects require further scrutiny or elaboration:

6.1 Distributor-Centric Approach

The consultation paper focuses on a distributor incentive of INR 500 after two years, effectively a carrot for those who help onboard new investors. While this helps expand outreach, it may inadvertently skew the distributor’s behavior:

Mis-selling or Churning Risks:

Distributors might aggressively push only certain schemes or orchestrate minimal compliance to earn the incentive.Uneven Impact Among Regions:

Large, well-established distributors in urban areas might still be the primary beneficiaries. The policy should explicitly encourage local, grassroots channels such as SHGs, microfinance institutions, or civil society groups more trusted by low-income communities.

6.2 Insufficient Financial Literacy Provisions

The proposal relies on existing channels for investor education, funded partially from the IEA Fund. Given that financial literacy is central to adoption, the policy needs a more robust and detailed plan for capacity-building at the grassroots level. Relying solely on mass messaging or text disclaimers might not fully equip first-time investors to handle market risks.

6.3 Absence of a Clear “Exit” Communication Strategy

While the consultation paper states that investors can exit without penalty, it offers no framework for ensuring that redemption is an informed choice. Distributors might be incentivized only at the point of sale, leaving the burden of exit decisions on financially less literate investors.

7. What Should Be Enhanced: Recommendations from Annexure A and Beyond

Annexure A of the Consultation Paper provides granular detail on operationalizing the scheme. Below are recommendations aligned with, and expanding upon, these details:

Wider Scheme Availability with Guidelines

Debt and Hybrid Options: Instead of a blanket exclusion of debt schemes, SEBI could allow certain short-duration or dynamic bond funds with historically stable returns. This gives investors more choice aligned with their time horizon and risk appetite, especially with the current market volatility (January 2025).

Smart Defaults: Offer curated “model portfolios” (e.g., 60% equity, 40% debt) or auto-rebalancing features for novices.

Graduated Approach to Limit Caps

Increasing SIP Caps Over Time: Instead of permanently restricting small-ticket SIP to INR 250, allow scaling to INR 500 or INR 1,000 after the investor has demonstrated consistent monthly deposits for, say, one year.

Tiered Incentives: Reduce management fees or offer partial expense ratio waivers to encourage investors to increase their monthly SIP amounts over time.

Strengthening Financial Literacy Programs

Localized Training: Mandate that at least part of the IEA Fund be allocated toward on-ground financial literacy camps in rural and urban low-income neighborhoods.

Digital Literacy Components: Many new investors will be using UPI autopay for the first time. Training in using smartphones securely is as crucial as learning about SIP basics.

Collaboration with Grassroots Intermediaries

Partnership with entities like BCNMs (Business Correspondent Network Managers) working closely with potential clients: These community-based organizations have a deeper understanding of local culture, trust, and credit behavior. They can be leveraged to explain the nuance of mutual funds, risk profiles, and the power of compounding.

Incentivize Local Champions: In addition to professional distributors, local “champions” (trained volunteers or NGO representatives) could be rewarded for continued investor engagement and mentorship.

Exit Support and Risk Mitigation

Guided Redemption: Provide an optional “exit counseling” service to ensure investors understand the implications of premature withdrawal. This helps minimize reactionary redemptions driven by short-term market fluctuations.

Micro-Insurance Add-On: Pair small-ticket SIPs with optional micro-insurance coverage so that sudden financial shocks do not derail the investor’s SIP habit entirely.

8. What Should Be Omitted or Pursued with Caution

In the pursuit of inclusive finance, well-intentioned policies can still lead to pitfalls. Here are potential areas of caution:

Aggressive Marketing Hype

Mutual funds, especially equity-driven products, carry risk. If the markets correct sharply, overpromising returns to vulnerable segments might result in negative publicity and erosion of trust.Mandatory Lock-In Periods

While the 5-year target is aspirational, a forced lock-in would be counterproductive. The program must remain open-ended to allow liquidity for emergencies, and a forced or penalized lock-in could deter participation.Uniform Approach Across Regions

India’s financial landscape is heterogeneous—what works in metro cities might not suit remote villages. A one-size-fits-all approach, implemented uniformly, might stifle local innovation. The regulation should allow tailored micro-campaigns or pilot projects.Complicated Red Tape

Reducing KYC costs and simplifying documents are essential. Any additional procedural requirement (like overly complex disclaimers or too many sign-offs) can scare off or confuse new investors.

9. Potential Impact on Building Financial Resilience in Low-Income Communities

9.1 Strengthening Household Safety Nets

The immediate benefit of microsavings in mutual funds is to build a gradual corpus. Even INR 250 per month, over five years, can accumulate into a significant sum (especially if invested in a balanced equity fund). This corpus is a buffer during personal emergencies—health crises, job loss, or natural disasters.

9.2 Behavioral Transformation

SIPs encourage discipline. For many in low-income segments, the notion of disciplined monthly saving—and viewing that money as an investment rather than a short-term transaction—can be a mindset shift. Over time, they may even pursue more advanced investments, insurance products, or entrepreneurial financing.

9.3 Long-Term Wealth Creation

If the scheme gains traction, it fosters inter-generational wealth. Children of today’s small-ticket SIP investors might inherit a basic familiarity with market-based instruments, bridging the generational gap in financial literacy and wealth accumulation.

9.4 Alternative credit score enhancement

Enables credit bureaus to include these as a part of the client's credit score, allowing a much more informed decision on the fiscal discipline of the client.

9.5 Unintended Consequences

Risk of Misselling and Overexposure: If distributors push equity funds without adequately explaining market volatility, communities might be blindsided by losses in a downturn.

Systemic Mistrust if Returns Fluctuate: Any significant market correction in the initial years could dampen enthusiasm and breed mistrust, tarnishing the concept.

10. Semi-final Word

Sachetising mutual fund investments at INR 250 per SIP can potentially become a powerful catalyst for financial inclusion in India. It directly tackles the affordability barrier, enabling millions of low-income individuals to invest in regulated, professionally managed funds—an opportunity once seen as exclusive to wealthier or more financially literate groups.

Global lessons underscore that technology-enabled micropayments, thoughtful regulation, and robust financial literacy campaigns form the backbone of such successful initiatives. SEBI’s Consultation Paper addresses several of these points, proposing a discounted cost structure, partial KYC reimbursement from the Investor Education and Awareness Fund, and a modest commission for distributors. By restricting small-ticket SIPs to Growth options and specific equity categories, the framework also aims to simplify the investment choice for first-time participants.

Yet, the paper leaves critical questions unaddressed. Are we inadvertently limiting diversification by excluding debt and thematic schemes? Will capping small-ticket SIPs at three hamper an investor’s growth if they wish to exceed the initial threshold? Who ensures that financial literacy goes beyond mere compliance? And how do we prevent misaligned distributor incentives or exploitative practices?

Annexure A provides deeper operational details, but future guidelines should incorporate flexible scheme choices, ensure tiered expansions for small-ticket SIP amounts, and implement robust on-ground financial literacy programs. Partnerships with grassroots organizations—be it BCNMs, self-help groups or microfinance institutions—will be crucial. Further, a structured approach to redemption counseling could safeguard novice investors from knee-jerk reactions and help them stay invested longer.

The potential gains for India’s low-income communities are significant. If managed well, micro-investments can expand the risk-absorbing capacity of vulnerable households, help them hedge against inflation, and potentially escalate them into mainstream financial prosperity. As more households gain discretionary resources, this can have transformational effects on everything from education to women’s empowerment.

Stakeholder feedback—especially from grassroots-level implementers, distributors, and communities—should guide SEBI in refining the final policy. In a country where over 60% of the population remains outside robust market-linked financial products, every rung on the ladder of financial inclusion counts. Sachetised mutual funds could well be the rung that scales India’s inclusive finance agenda to unprecedented heights.